Over the past two years, AI has become the core driver of growth in the technology industry.

GPUs, HBM, and advanced packaging attract most of the market attention in computing chips.

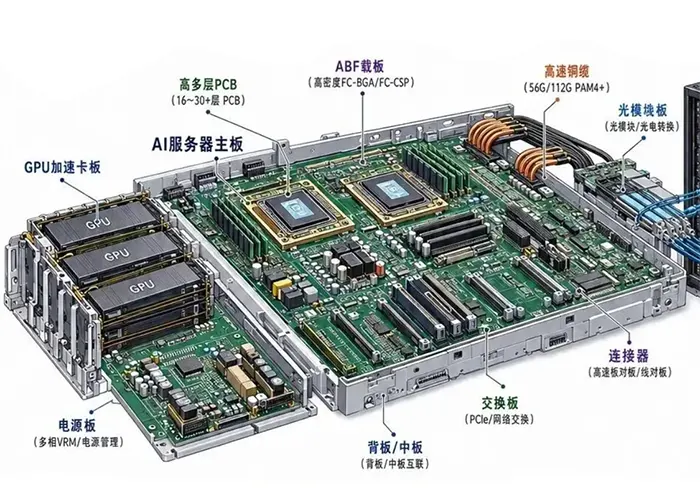

However, foundational electronic components and materials—such as PCBs, CCLs, ABF substrates, testing equipment, and passive components—form the core that drives the ongoing evolution of AI computing infrastructure.

As AI server performance continues to improve—with larger chip areas, rising power consumption per rack, and increasing packaging complexity—the electronics supply chain is undergoing a profound restructuring of value.

Basic components, once viewed as merely supporting elements, have now become key bottlenecks constraining the pace of AI industry development, while also creating highly certain growth opportunities.

The changes brought about by AI are not limited to growth in demand volume; they are also reflected in a significant increase in the value per unit.

High-end PCBs and M9/M10-grade CCLs advance in step with AI infrastructure upgrades. ABF substrate boards, T-Glass materials, SLT test equipment, CPO testing, and data center power supply testing also evolve alongside these system improvements.

Each of these segments shifts from a supporting position in the supply chain toward a more central and leading role in industry development.

AI Propels PCB/CCL into a Super Growth Cycle

Projections:

- The HPC (High-Performance Computing) CCL market size is expected to grow from approximately $3.9 billion in 2025 to nearly $10 billion in 2027

- The compound annual growth rate (CAGR) for 2025–2027 is approximately 60%

The driving force behind this is the explosive growth in the value of AI servers

As Nvidia’s Blackwell, Rubin, Rubin Ultra, Google TPU, and AWS Trainium continue to evolve, AI servers are featuring an increasing number of PCB layers; board grades are upgrading from M7 to M8, M9, and even M10; CCL usage per chip continues to rise; and the value of CCL per server cabinet has surpassed the $200,000 mark.

Consequently, the PCB industry no longer relies on growth in shipment volume but rather on the increase in value driven by AI platform upgrades.

Supply Shortage May Emerge for High-End PCBs and CCLs

The difficulty of manufacturing AI PCBs is rising sharply. The increase in layer count, greater HDI complexity, and the upgrade to M9/M10 board materials are putting sustained pressure on manufacturing yields.

At the same time, CCL production capacity is expanding only slowly, and high-end materials rated M9 and above are in short supply.

In the coming years, supply growth for AI server PCBs and high-end CCL may lag behind demand growth, potentially leading to a prolonged state of supply-demand tension for high-end PCBs and CCL.

IC Substrates Are Set to Enter a Historic Period of Supply Shortages

Assessment: The AI substrate industry is about to enter an unprecedented period of scarcity

Three reasons for this:

1. AI chip sizes are expanding rapidly

For example, the package areas of Hopper, Blackwell, Rubin, Rubin Ultra, and Feynman continue to grow.

In the future, GPU substrate areas may reach several times the size of current products.

2. CoWoS continues to scale up

Gradually upgrading from 1.5x reticles to 12x reticles

Substrate sizes are expanding accordingly.

3. AI’s share of demand is rising rapidly

The report forecasts that by 2028:

- AI servers and switches will account for 75% of global substrate demand

- Becoming the dominant market segment

With a compound annual growth rate (CAGR) of approximately 67% from 2025 to 2028.

T-Glass will become one of the most scarce materials in the AI era

Special note:

T-Glass (ultra-low thermal expansion glass fiber fabric) may become a major bottleneck limiting the expansion of substrate production.

Reasons:

AI substrate sizes are growing larger, warpage control requirements are becoming stricter, and high-end ABF substrates are increasingly adopting T-Glass.

Meanwhile, global supply is highly concentrated.

Consequently:

- Long-term agreements (LTAs) are beginning to emerge

- The capacity reservation model is gaining traction

- Leading companies’ bargaining power is increasing

It is believed that T-Glass supply shortages may become one of the biggest variables in the substrate industry chain in the coming years.

AI Test Equipment Enters a Second Growth Curve

Test equipment manufacturers, led by Chroma, have benefited significantly.

From Hopper to Blackwell and Rubin, GPU testing times have continued to lengthen due to higher power consumption, more complex chips, and stricter system validation requirements.

Demand for SLT (System-Level Test) equipment is increasing, and the average selling price of test equipment is rising, creating a scenario of growth in both volume and price.

CPO (Co-Packaged Optics) expands the scope of testing into a new market segment.

Silicon photonics, optical engines, and CPO technologies gain broader adoption across AI systems.

This adoption drives new requirements, including optical module testing, optical engine testing, and combined ASIC+CPO testing, which together shape an entirely new market for test equipment.

AI Data Center Power Supply Testing Emerges as a New Blue Ocean

Power consumption in AI server racks has surged from several kilowatts to tens of kilowatts or even higher, driving explosive demand for equipment such as PSUs, HVDCs, BBUs, and Power Racks.

The AI server power supply market is projected to maintain a growth rate of over 80% in the coming years, making the corresponding power supply testing equipment and data center power supply testing platforms one of the fastest-growing segments in the testing industry.

Passive Components Such as MLCCs Enter a New Growth Cycle

AI servers require far more MLCCs than traditional servers due to higher power consumption, more complex power distribution networks, and a greater number of power management modules.

The increased use of MLCCs per server, combined with rising industry shipments and stable average selling prices, is collectively propelling the passive component industry into a new growth cycle.

Conclusion

The AI era is fundamentally reshaping the entire electronics supply chain, shifting value creation from isolated high-performance chips toward a much broader and more complex infrastructure ecosystem.

AI servers continue scaling in compute density, power consumption, and packaging complexity, driving rapid changes in system design requirements.

PCBs, CCLs, ABF substrates, T-Glass materials, testing equipment, and passive components increasingly determine overall system performance and scalability.

What was once a support layer in the industry is now moving to the center of value creation.

High-layer HDI PCBs, advanced copper-clad laminates, large-scale IC substrates, and next-generation testing and power systems collectively face tightening structural supply constraints.

These segments simultaneously experience a rapid increase in unit value, while technological barriers continue to rise at an accelerating pace across the industry.

Looking ahead, the imbalance between accelerating AI-driven demand and relatively slow supply expansion in high-end materials and manufacturing capacity is likely to persist.

This will not only sustain pricing power across key segments but also reinforce a long-term upgrade cycle throughout the entire electronics ecosystem.

Within the AI infrastructure boom, companies positioned in high-barrier and high-reliability segments of the supply chain are gaining the strongest advantages.

Precision materials, advanced manufacturing capabilities, and system-level testing technologies are rising in importance and now rival compute itself in determining overall system performance and industry leadership.